Advice for First-Time Home Buyers

Buying your first home is exciting. And scary. And thrilling. And overwhelming. All at once.

If you’re a First Time Home Buyer, you’re stepping into one of the biggest financial decisions of your life. The good news? You don’t have to figure it out alone. With the right plan and guidance, the process becomes less stressful and far more rewarding.

Before we dive in, here’s a quick overview of what truly matters.

Overview: Key Advice for Every First Time Home Buyer

Know your real budget – Understand what you can afford before you fall in love with a house.

Prepare your credit and finances early – Lenders look closely at your financial story.

Explore loan and assistance programs – Many first-time buyers qualify for special options.

Work with experienced professionals – A knowledgeable lender and agent make all the difference.

First Time Home Buyer: Start With a Clear Budget

If you’re a First Time Home Buyer, the very first step is simple: know what you can truly afford.

Not what you hope you can afford.

Not what the online calculator says at a glance.

But what fits comfortably into your real life.

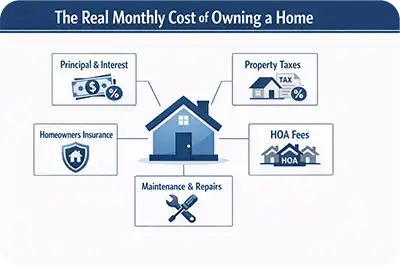

Why Budgeting Matters More Than You Think

A mortgage isn’t just a monthly payment. It includes:

Principal and interest

Property taxes

Homeowners insurance

HOA fees (if applicable)

Maintenance and repairs

Think of homeownership like owning a car. You don’t just pay for gas. There’s insurance, oil changes, tires, and the occasional surprise repair. Homes are the same.

A safe rule? Keep your total housing payment within a range that allows you to:

Save monthly

Handle emergencies

Enjoy life without constant stress

No house is worth losing sleep over.

Understand Your Credit Score Before Applying

Your credit score tells lenders how risky you are as a borrower. The higher your score, the better your loan options.

As a First Time Home Buyer, improving your credit even slightly can:

Lower your interest rate

Reduce your monthly payment

Increase your approval chances

Simple Ways to Strengthen Your Credit

Pay bills on time (every time)

Keep credit card balances low

Avoid opening new accounts before applying

Check your credit report for errors

You can review your credit report for free at AnnualCreditReport.com, a service authorized by the federal government.

Even a small boost in your score can save thousands over the life of a loan. Isn’t that worth a little preparation?

Save More Than Just the Down Payment

Many First Time Home Buyers focus only on the down payment. But there are other costs you need to prepare for.

What Else Should You Budget For?

Closing costs (usually 2–5% of the home price)

Home inspection fees

Appraisal fees

Moving expenses

Initial repairs or updates

Let’s say you buy a home and move in. Then the water heater fails two weeks later. It happens. Having an emergency cushion protects you from panic.

A healthy savings plan includes:

Down payment

Closing costs

3–6 months of emergency expenses

Preparation equals confidence.

Explore First-Time Buyer Loan Programs

Here’s something many people don’t realize:

There are loan programs designed specifically for the First Time Home Buyer.

These programs can offer:

Lower down payment requirements

Flexible credit guidelines

Competitive interest rates

Down payment assistance

Common Loan Options

Many first-time buyers qualify for programs they didn’t know existed. Conventional loans

FHA loans

VA loans (for eligible veterans)

USDA loans (for eligible rural properties)

Many states and local governments also offer assistance programs. You can explore official federal resources at HUD.gov, which provides information about homebuyer programs and counseling.

Don’t assume you don’t qualify. Ask. You might be pleasantly surprised.

Get Pre-Approved Before House Hunting

Picture this:

You find your dream home.

You fall in love.

You make an offer.

But another buyer already has financing lined up.

That’s tough.

Getting pre-approved shows sellers you’re serious. It also helps you:

Know your exact price range

Shop with confidence

Avoid wasting time on homes outside your budget

Pre-approval is not the same as pre-qualification. Pre-approval involves verifying income, assets, and credit. It carries weight.

For a First Time Home Buyer, this step turns guesswork into clarity.

Work With the Right Real Estate Professionals

Buying your first home isn’t a DIY project.

You need:

A knowledgeable lender

A trustworthy real estate agent

Possibly a real estate attorney (depending on your state)

These professionals guide you through:

Offer negotiations

Contract terms

Inspection responses

Closing paperwork

Think of them as your home-buying team.

Choose professionals who:

Explain things clearly

Answer questions patiently

Communicate consistently

Have experience with first-time buyers

The right team reduces stress dramatically.

Don’t Skip the Home Inspection

A house can look perfect. Fresh paint. New flooring. Bright kitchen.

But what’s behind the walls?

A home inspection helps uncover:

Structural issues

Roof problems

Plumbing concerns

Electrical hazards

As a First Time Home Buyer, you might feel tempted to waive inspections in a competitive market. That’s risky.

An inspection gives you:

Negotiation power

Repair requests

Peace of mind

It’s like getting a medical checkup before making a lifelong commitment.

Think Long-Term, Not Just Right Now

It’s easy to focus on what you want today.

But ask yourself:

Will this home fit your needs in five years?

Is the neighborhood growing?

How is the school district?

What about resale value?

Buying a home is part financial decision, part lifestyle decision.

A First Time Home Buyer should consider:

Commute times

Future family plans

Job stability

Local market trends

The right home isn’t just beautiful. It’s practical.

Understand the True Cost of Homeownership

Owning a home feels empowering. But it also brings responsibility.

Here’s what changes:

You fix the leaks

You replace the appliances

You maintain the yard

No landlord. No maintenance hotline.

That said, homeownership also builds:

Equity over time

Stability

Long-term wealth potential

It’s a trade-off. Responsibility in exchange for ownership.

And for many, it’s absolutely worth it.

Avoid Major Financial Changes Before Closing

This is critical advice for any First Time Home Buyer.

Once you’re under contract:

Don’t open new credit cards

Don’t finance a car

Don’t change jobs without discussing it

Don’t make large unexplained deposits

Lenders re-check your financial situation before closing. A sudden change can delay or even cancel your loan approval.

Stay steady. Finish strong.

Frequently Asked Questions

How much should a First Time Home Buyer save before purchasing?

Most experts recommend saving at least 3–5% for a down payment, plus closing costs and an emergency fund. More savings provides greater flexibility and peace of mind.

What credit score does a First Time Home Buyer need?

It depends on the loan type. Some programs allow scores in the mid-600s or even lower, but higher scores generally qualify for better rates.

Are there grants for First Time Home Buyers?

Yes, many state and local programs offer grants or down payment assistance. Eligibility varies based on income, location, and property type.

How long does the home buying process take?

From pre-approval to closing, the process often takes 30–60 days once you’re under contract. Preparation before house hunting can take longer.

Is renting better than buying?

It depends on your goals. Buying builds equity over time, while renting offers flexibility. The right choice depends on your financial situation and long-term plans.

What is the biggest mistake First Time Home Buyers make?

One of the biggest mistakes is buying more house than they can comfortably afford. Sticking to a realistic budget prevents financial strain later.

Final Thoughts for Every First Time Home Buyer

Becoming a First Time Home Buyer is a milestone. It’s a mix of excitement, nerves, and big decisions.

But here’s the truth:

Preparation changes everything.

When you:

Understand your finances

Explore your loan options

Work with the right professionals

Think long-term

…you move from anxious to confident.

Buying your first home isn’t just about property. It’s about building a future. With smart planning and the right advice, that future starts strong.

And that? That’s a powerful feeling.